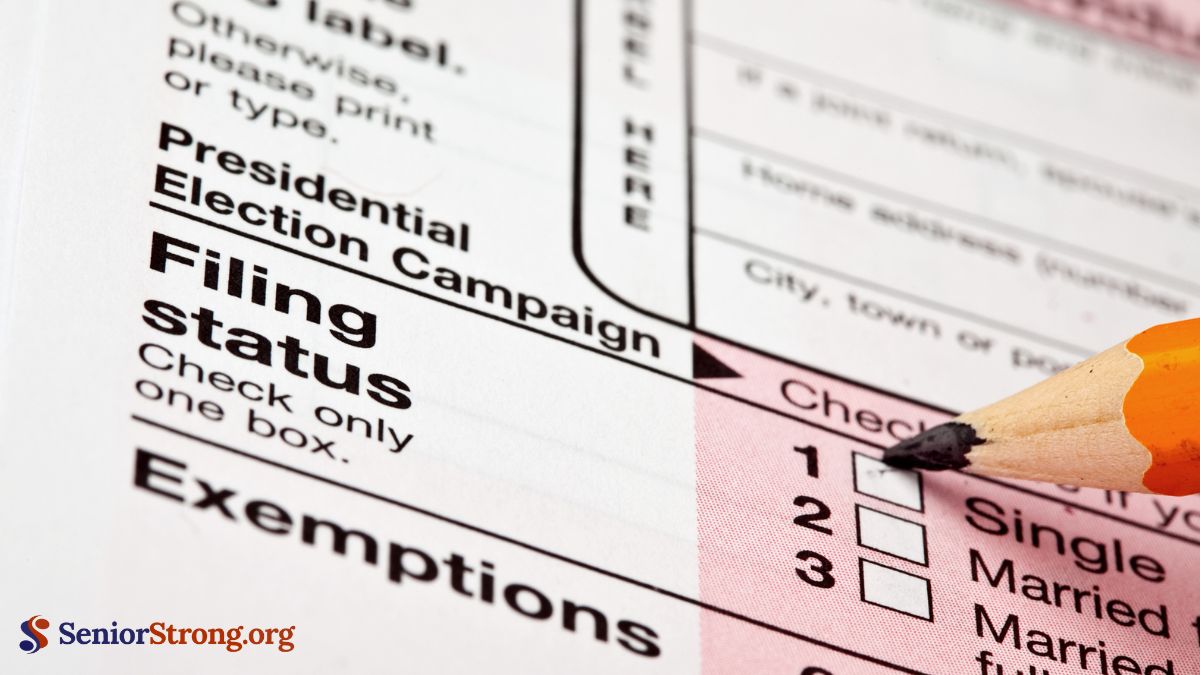

As a retired individual, it's important to consider your filing status options to effectively manage your tax situation and maximize benefits. You typically have three main choices: Single, Married Filing Jointly, or Head of Household.

Filing jointly often allows for higher income thresholds and access to more deductions. For example, according to the IRS, couples filing jointly may benefit from a larger standard deduction, which can help reduce taxable income.

On the other hand, if you file as Single, you might face higher tax rates, particularly if your income is within certain brackets.

If you're caring for dependents, you might want to look into the Head of Household status. This option generally provides a larger standard deduction and lower tax rates, which can be quite beneficial.

According to historical data, individuals who qualify as Head of Household often see a significant reduction in their tax burden compared to those filing as Single.

Each of these options can impact your overall tax liability and should be evaluated based on your specific retirement income sources, such as pensions, Social Security, and investments.

It's always a good idea to crunch the numbers for each scenario, as the right choice can lead to substantial savings. Stay tuned for more valuable insights that can help you navigate your tax decisions effectively!

Retired individuals have several options for filing their taxes, including Single, Married Filing Jointly, Married Filing Separately, and Head of Household. Each status has its own benefits, depending on your personal circumstances.

For instance, if you file as Single, you can take advantage of a standard deduction of $13,850, which is particularly beneficial for those over 65, as they can claim an additional deduction. On the other hand, if you're married and choose to file jointly, you may find greater income thresholds, along with access to various deductions and credits that can help reduce your overall tax burden.

If you qualify for Head of Household status, you can enjoy a higher standard deduction and lower tax rates. This option is available to those who support dependents and meet specific criteria, making it an appealing choice for eligible retirees.

It's crucial to carefully evaluate your unique financial situation to ensure you're maximizing your tax benefits while minimizing your liabilities. This might involve consulting with a tax professional or doing some research to understand which filing status would be most advantageous for you.

When it comes to filing your taxes, understanding your options is crucial, especially for retirees. Your filing status can significantly influence your tax implications and how your retirement income is taxed. Knowing which status best fits your situation can help you navigate the tax landscape more effectively.

As a retiree, you typically have a few filing status options: Single, Head of Household, or Married Filing Jointly. Each choice presents its own set of advantages and disadvantages. For instance, if you're married, filing jointly often allows you to benefit from higher income thresholds before reaching certain tax brackets. This can be particularly helpful in minimizing your tax liability.

On the other hand, if you're single, you might appreciate the simplicity of filing as a Single taxpayer despite potentially facing higher tax rates.

It's also essential to evaluate your retirement income sources—whether it's Social Security, pensions, or withdrawals from retirement accounts—as these can impact your overall tax burden. For example, according to the IRS, up to 85% of your Social Security benefitsBenefits provided under the Social Security Act, including retirement income, disability income, Med... may be taxable, depending on your overall income.

If you're filing as a Single taxpayer, there are some important tax implications to consider that can impact your financial health during retirement. One significant factor is how your retirement income is taxed. Unlike married couples, who can benefit from combined income thresholds, Single filers may find themselves facing higher tax rates on their retirement benefits due to these separate thresholds.

To optimize your tax situation, it's crucial to maximize your deductions, particularly if you have medical expenses or other qualifying costs. As a Single filer, you can take advantage of the standard deduction, which, for the tax year 2023, is $13,850. This deduction can significantly lower your taxable income, offering a valuable financial cushion.

If you're over the age of 65, there's good news: you can claim an additional deduction, which enhances the potential tax savings.

It's also essential to organize your retirement income sources, such as Social Security and pensions.

While being a Single filer may come with its challenges, it also provides an opportunity to tailor your financial strategies to your personal circumstances. Staying informed and proactive about your tax situation can help you enjoy a more secure and fulfilling retirement.

When it comes to tax filing, married couples often find that choosing to file jointly can lead to substantial benefits, especially as they approach retirement. According to the IRS, when you and your spouse file together, you generally benefit from a higher combined income threshold before entering the higher tax brackets. This allows you to retain more of your hard-earned income.

Filing jointly also opens the door to various deductions and credits that you might miss out on if you decide to file separately. For instance, you could qualify for the Earned Income Tax Credit or enjoy a larger standard deduction, which effectively reduces your taxable income. This can have a significant impact on your financial landscape during retirement.

The Tax Policy Center notes that married couples who file jointly often see lower overall tax liabilities compared to those who file separately.

Additionally, the convenience of filing a single joint return simplifies the tax preparation process. Instead of completing two separate returns, you only need to fill out one, saving you time and effort. Working as a team can make navigating the complexities of taxes much more manageable.

Deciding to file your taxes as Married Filing Separately can sometimes appear to be the simpler route, especially if you and your spouse have significant differences in income or deductions.

However, it's essential to carefully consider the tax implications of this choice. While it might streamline certain aspects of your tax situation, it can also restrict potential benefits.

Here are three key factors to keep in mind:

Ultimately, weighing these factors against your unique financial situation can help ensure you make the best decision for your circumstances.

Taking the time to evaluate your options can lead to more informed tax planning and potentially save you money in the long run.

Head of Household status can be a great option for retired individuals who qualify, providing a higher standard deduction and potentially lower tax rates than filing as a single. To benefit from this status, you need to meet specific requirements.

First, you must be unmarried or deemed unmarried on the last day of the tax year. Additionally, you should have paid more than half the costs of maintaining a home for yourself and your qualifying dependents.

Qualifying dependents can include children, stepchildren, or some relatives who live with you and depend on your support. This not only enhances your tax benefits but also fosters a sense of community and belonging, as you're supporting those you care about.

If you find that you're eligible for Head of Household status, it's definitely worth looking into. This filing status could ease your tax burden, and it reflects your role as a caregiverAn individual who provides care to someone who needs help with daily tasks and activities due to chr..., which can deepen your connection with your loved ones.

Plus, every dollar saved in taxes can be redirected toward enjoying your retirement even more. So, take the time to evaluate your situation and see if this option is a good fit for you.

Yes, retirees can claim deductions for medical expenses if their qualifying medical expenses exceed 7.5% of their adjusted gross income (AGI). This deduction can be quite beneficial as it helps alleviate some of the financial pressures associated with healthcare costs during retirement. It's important to keep thorough records of all medical expenses, as only those that qualify can be considered for this deduction. If you're looking for more detailed information, resources like the IRS website or major financial news outlets can provide comprehensive guidance on this topic.

Social Security benefits can definitely play a role in determining your filing status when it comes to taxes. According to the IRS, if your combined income—which includes your adjusted gross income, any nontaxable interest, and half of your Social Security benefits—exceeds certain thresholds, it may push you into a higher tax bracket.

For instance, for individuals, if your combined income is between $25,000 and $34,000, you may have to pay taxes on up to 50% of your Social Security benefits. If it exceeds $34,000, up to 85% of your benefits could be taxable. This is important because understanding these thresholds can help you make informed decisions about your deductions and overall tax strategy.

Yes, there are indeed tax credits available for retired individuals. You may qualify for certain credits based on your retirement income, which can significantly help reduce your tax burden. For instance, the Credit for the Elderly or the Disabled is one such benefit available to seniors, which can increase your financial security. It's always a good idea to check with the IRS or consult with a tax professional to understand your eligibility and maximize your benefits.

Filing jointly after a divorce can really impact your tax situation in some significant ways. According to various tax experts and resources like the IRS and financial planning websites, there are potential benefits such as lower tax rates and eligibility for certain deductions, which can be quite appealing. However, it's important to tread carefully.

For instance, if you file jointly, it could potentially influence your divorce settlement or future financial arrangements. This is because your combined income might change the way assets and debts are divided. Additionally, if one spouse has tax liabilities or issues, the other might be held responsible, which can complicate things further.

Yes, you can change your filing status after submitting your return, but there are a few important things to consider. The IRS allows you to amend your tax return using Form 1040-X. However, changing your filing status can have various implications on your tax liabilities and potential refunds.

For example, if you switch from "Married Filing Jointly" to "Married Filing Separately," you might lose out on certain tax credits and deductions that are only available to joint filers. On the other hand, if you were eligible for a different status like "Head of Household," it could result in a lower tax rate and a higher standard deduction.

It's always a good idea to fully understand the consequences of changing your filing status. Consulting a tax professional can provide valuable insights based on your unique financial situation. They can help you navigate the complexities of the tax code and ensure that you're making the best decision for your circumstances.