Social Security tax plays a significant role in how retirees manage their finances, and it's essential to understand its impact. During your working years, you contribute to Social Security through FICA taxes, which are designed to fund your future benefits.

However, once you retire, the taxes on your Social Security benefitsBenefits provided under the Social Security Act, including retirement income, disability income, Med... can vary based on your total income. If your combined income exceeds certain IRS thresholds, you could end up paying taxes on your benefits. In fact, for some retirees, up to 85% of their Social Security benefits may be taxable.

This can significantly reduce your disposable income, making it crucial to plan accordingly. Understanding these tax implications can help you make informed financial decisions as you prepare for retirement.

It's wise to consider how your overall income willA legal document that states how a person's property should be managed and distributed after death. be affected by these taxes, so you can create a solid retirement income strategy. By reflecting on these factors, you can better navigate the complexities of retirement finances and ensure that your hard-earned benefits work for you.

Understanding the Social Security tax is crucial for anyone planning for retirement. It's important to be informed about how these taxes function, as they significantly impact your future benefits.

Social Security taxes are primarily collected through the Federal Insurance Contributions Act (FICA), which ensures that funds are available for retirees like you.

As of 2023, the Social Security tax rate is set at 6.2% on earnings up to a wage base limit of $160,200. This limit is adjusted annually based on changes in national average wage levels.

Every paycheck you receive contributes to your future benefits, effectively building a safety net for when you retire. Though the numbers might seem confusing at first, understanding how these tax rates influence your benefits can empower you to make informed decisions about your financial future.

It's also worth noting that Social Security isn't just about the numbers; it's about becoming part of a community of retirees who depend on these benefits.

Navigating the taxation on Social Security benefits can seem daunting, but it's crucial for retirees to grasp how it operates. Understanding the taxable income derived from your benefits can significantly enhance your financial planning. Depending on your total income, it's possible for a portion of your Social Security benefits to be taxable.

The Internal Revenue Service (IRS) has established specific income thresholds that dictate whether you'll need to pay taxes on your Social Security income. If your combined income exceeds these limits, you could be taxed on as much as 85% of your benefits. This "combined income" is calculated by adding your adjusted gross income, any nontaxable interest, and half of your Social Security benefits.

For many retirees, monitoring your overall income can greatly influence your tax situation. You might want to consider strategies to manage your taxable income, such as modifying withdrawals from retirement accounts or looking into tax-efficient investment options.

This proactive approach can help you enjoy your retirement without the worry of unexpected tax liabilities. Remember, you're not alone in navigating these complexities; many retirees face similar hurdles, and sharing experiences can lead to discovering effective solutions together.

Managing your Social Security benefits is crucial for ensuring a comfortable retirement income. A good understanding of how Social Security fits into your overall retirement plan is essential. Failing to consider the tax implications of your benefits could lead to less disposable income than you might expect.

Social Security often serves as a foundation for retirement income, but it's important to remember that it shouldn't be your sole source. According to the Social Security Administration, many retirees rely on a combination of Social Security, pensions, savings, and investments to maintain their standard of living. This diversified approach can help create a more stable financial future.

When planning your retirement income, timing can be everything. For instance, if you decide to take your Social Security benefits early, your monthly payments will be reduced, which can have lasting effects on your financial well-being. A report from the National Bureau of Economic Research highlights that this decision can significantly impact your total lifetime benefits. By being proactive and strategic about when to claim your benefits, you can maximize what you receive and improve your overall financial situation.

It's also wise to consider how your Social Security benefits interact with other income sources. For example, your benefits may be subject to taxes if your combined income exceeds certain thresholds, as outlined by the IRS. This could further affect your disposable income during retirement.

By understanding these factors, you not only enhance your own financial literacy but also foster a sense of community with others navigating similar challenges. Sharing insights and supporting one another can make a significant difference in your retirement planning journey.

Adjusting your Social Security benefits due to additional income can have a significant impact on your financial situation during retirement. It's important to understand how your earnings interact with various income thresholds and tax brackets so you can make informed decisions.

Here are four key points to consider:

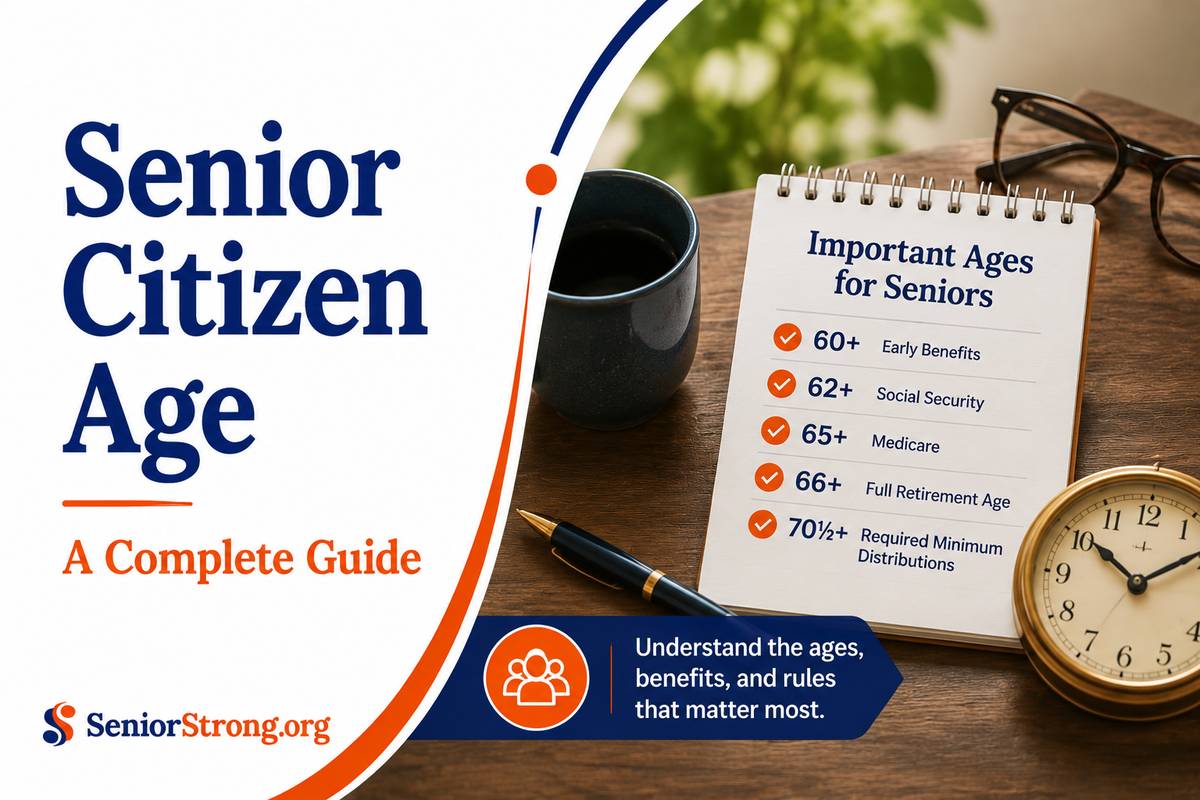

1. Income Limits: If you're below your full retirement age, exceeding certain income thresholds can lead to a reduction in your Social Security benefits. According to the Social Security Administration (SSA), in 2023, for every $2 you earn over the limit ($21,240), your benefits will be reduced by $1.

2. Tax Implications: Earning additional income can elevate you into a higher tax bracket, which in turn affects your overall tax burden. The IRS has progressive tax rates, meaning that the more you earn, the higher the percentage you pay on your income. This can be especially relevant for retirees who may not have previously earned enough to be taxed at a higher rate.

3. Benefit Adjustments: The SSA may adjust your monthly benefits if your income exceeds specific thresholds. For retirees under full retirement age, this can mean a temporary reduction in benefits until you reach that age.

Once you reach full retirement age, your benefits can be recalculated to reflect any withheld amounts.

4. Long-Term Planning: It's wise to think about how any additional income may affect your future benefits, particularly if you plan to continue working while drawing Social Security. Understanding these dynamics can help you strategize your retirement income more effectively.

When it comes to minimizing the tax impact of your Social Security benefits and additional income during retirement, there are several effective strategies you can consider. One key approach is to prioritize tax-efficient withdrawals from your retirement accounts. By carefully choosing which accounts to draw from—such as Roth IRAs versus traditional IRAs—you can manage your taxable income more effectively. This can help you preserve your Social Security benefits and avoid unnecessary taxation.

Investment diversification is another important strategy. By spreading your investments across various asset classes, you can't only protect your portfolio from market volatility but also create income streams that are more tax-efficient. For example, investing in municipal bonds can provide you with tax-free interest, while dividends from qualified stocks are often taxed at a lower rate than ordinary income.

Additionally, it's beneficial to explore other income sources that mightn't count towards your combined income, such as certain part-time work or specific types of annuities. By taking a proactive approach and implementing these strategies, you can create a financial landscape that feels more secure and less burdened by taxes.

Social Security tax for retirees is determined by looking at your taxable income, which encompasses wages, pensions, and other sources of earnings. The way your benefits are calculated takes these factors into account, ultimately influencing the amount of tax you may owe on your Social Security benefits.

To break it down a bit more, the IRS considers your combined income, which is your adjusted gross income plus any tax-exempt interest and half of your Social Security benefits. Depending on this total, you may have to pay federal income tax on your benefits if your income exceeds certain thresholds. For instance, if you're filing as an individual and your combined income is between $25,000 and $34,000, you might pay taxes on up to 50% of your benefits. If it exceeds $34,000, up to 85% of your benefits could be taxable.

It's a bit of a balancing act, so keeping track of all your income sources is key as you navigate this part of retirement. Always consider consulting IRS guidelines or a tax professional for personalized advice, especially since tax laws can change!

Absolutely, retirees can receive Social Security benefits while still working. It's important to note, though, that if you earn more than a certain limit—around $19,560 in 2023—your benefits could be reduced. This is part of the Social Security Administration's rules intended to balance work and benefits. So, if you're considering working while receiving Social Security, it's a good idea to evaluate your financial situation and see how your earnings might impact your benefits. It's always wise to stay informed and plan accordingly!

If you choose to delay your retirement, you'll actually see an increase in your Social Security benefits. This is because for each year you postpone taking your benefits past your full retirement age, your monthly payment can rise by a certain percentage—typically around 8% for each year you delay until age 70. This can result in a significantly higher income later in retirement, which can enhance your overall retirement planning.

According to the Social Security Administration, this strategy allows many individuals to enjoy a more comfortable lifestyle during their later years. By waiting, you not only bolster your monthly checks but also potentially increase your total benefits over your lifetime, especially if you live into your 80s or 90s. So, delaying retirement can be a savvy financial move for many people, allowing them to maximize their benefits while enjoying a more secure financial future.

Yes, there are variations in Social Security tax rates by state, but it's important to clarify that the federal Social Security tax rate itself is uniform across the United States. As of now, it stands at 6.2% for employees and 6.2% for employers on earnings up to a certain limit, which is adjusted annually.

However, when it comes to state taxes, some states impose their own income taxes, which can affect your overall retirement income. For example, states like Florida and Texas do not impose a state income tax at all, potentially leaving more money in your pocket during retirement. Conversely, states with higher income tax rates can impact your retirement financial planning.

Additionally, some states may tax Social Security benefits differently. For instance, states like New York and Illinois do not tax Social Security benefits, while others, like California, may tax them under certain income thresholds.

Social Security tax can have a significant impact on spousal benefits, primarily by affecting the overall income and eligibility for benefits of both spouses. If one spouse has a higher income that is heavily taxed, this can influence the total benefits available to the couple.

For instance, Social Security benefits are calculated based on the highest 35 years of a person's earnings, and if a spouse earns more, it can lead to a higher benefit amount. However, if that income is heavily taxed, it could potentially influence decisions about when to claim benefits, as higher earners may want to delay claiming to maximize their benefits.

It's also important to note that spousal benefits can be up to 50% of the higher-earning spouse's benefit if claimed at full retirement age. Therefore, understanding how Social Security taxes impact your combined earnings and benefits can help you make more informed financial decisions for your future. It's always a good idea to consult with a financial advisor or use resources from the Social Security Administration to explore your specific situation.