There is no single age that makes you a senior citizen. The answer depends entirely on who is asking and why. You can claim restaurant and retail discounts at 50 or 55, qualify for federal Medicare health coverage at 65, and reach your full Social Security retirement age at 67 if you were born in 1960 or later. So the practical question is not “what age am I a senior?” but “which senior threshold matters for the decision in front of me right now?”

That distinction matters more in 2026 than it has in decades. This year marks the final scheduled step in raising the U.S. full retirement age to 67, a change confirmed by the Social Security Administration. This guide breaks down every age that confers “senior” status, why the numbers differ, and how to use each one.

A senior citizen is most commonly defined as someone aged 65 or older, but that number is a convention, not a rule. Commercial discounts can begin at 50, government health coverage starts at 65, and full retirement benefits now arrive at 67. The “right” age is the one attached to the specific benefit you want.

Researchers who study aging avoid pinning seniorhood to one birthday because chronological age is only one of several ways to measure it. Social gerontologists separate chronological age (the years you have lived) from biological age (how your body and mind actually function), life-stage age (markers like retiring or becoming a grandparent), and policy age (the legal thresholds that unlock pensions and health programs). A 60-year-old marathon runner and a frail 60-year-old are the same chronological age and worlds apart biologically.

Because these dimensions rarely line up, global health bodies have shifted toward measuring functional ability instead of counting birthdays. The World Health Organization now frames healthy aging around what a person can still do, not the number on their driver’s license. For everyday purposes, though, you willA legal document that states how a person's property should be managed and distributed after death. still run into fixed age cutoffs constantly, and knowing them saves real money.

Age 65 became the cultural shorthand for old age because of a policy decision made in Germany more than a century ago, not because anything biological happens at 65. The number was inherited, repeated, and eventually written into U.S. law.

Chancellor Otto von Bismarck introduced the world’s first national social insurance program in Germany in the 1880s. The original pension age was 70, then lowered to 65 in 1916. When the United States drafted the Social Security Act of 1935, it borrowed that German benchmark, and 65 lodged itself in the public mind as the entry point to old age. Medicare later adopted the same age, reinforcing it.

The irony is that 65 no longer matches the program it came from. As of 2026, you can get Medicare at 65 but cannot collect your full Social Security benefit until 67. The two halves of “retirement” have drifted two years apart, which is exactly why so many people are confused about when they actually become a senior in the eyes of the government.

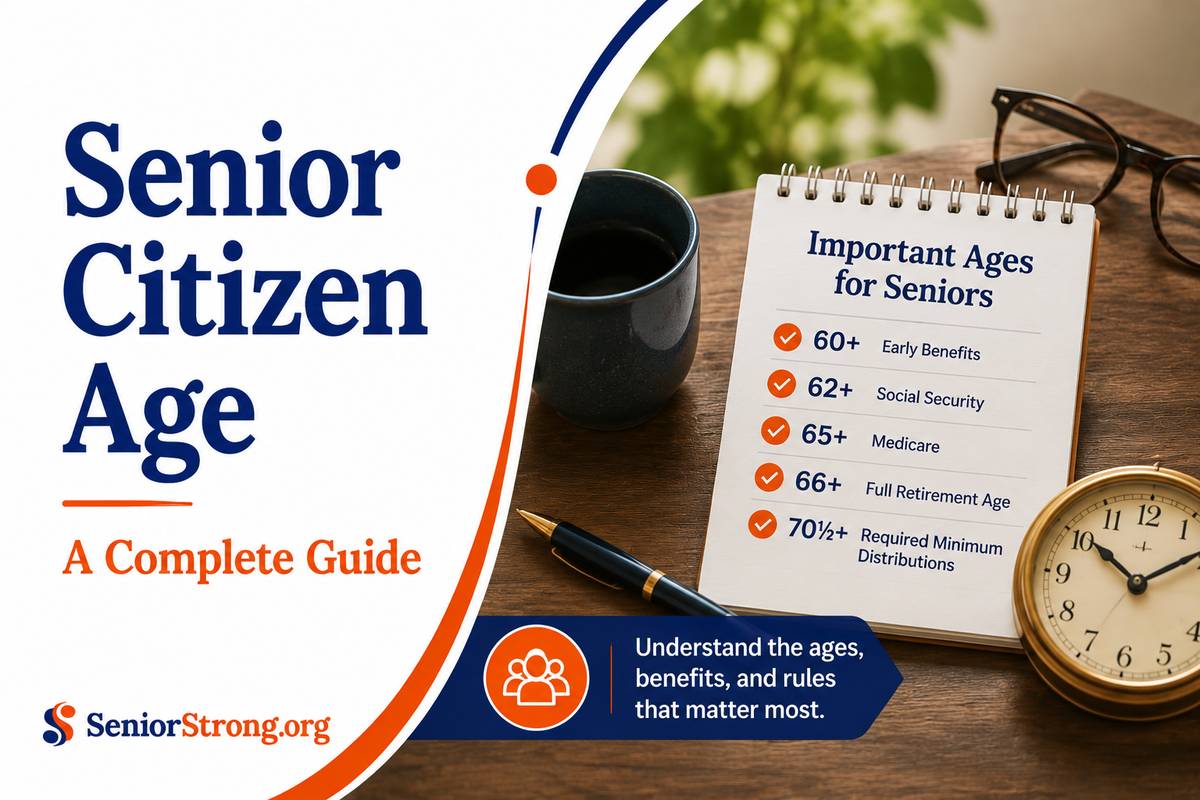

Senior age thresholds range from 50 to 67 depending on the country and the program. In the U.S., the key ages are 62 for early Social Security, 65 for Medicare, and 67 for full retirement. Internationally, pension ages cluster between 60 and 67.

The table below shows the major government age milestones by country, drawn from official pension and health agencies. Note how few of them actually land on 65.

| Country / Region | Key Age | Program or Context |

|---|---|---|

| United States | 62 | Earliest age to claim reduced Social Security retirement benefits |

| United States | 65 | Eligibility for federal Medicare health insurance |

| United States | 67 | Full Social Security retirement age for those born in 1960 or later |

| Canada | 65 | Eligibility for the Old Age Security (OAS) pension; CPP can start at 60 reduced |

| United Kingdom | 67 | State Pension age, phasing up from 66 between April 2026 and April 2028 |

| Australia | 67 | Age Pension eligibility; Seniors Card available earlier (often 60) |

| United Arab Emirates | 60 | Official threshold for senior citizen status and benefits |

| United Nations / WHO | 60+ | Global standard definition of “older persons” |

Sources: U.S. figures from the Social Security Administration; UK timeline confirmed by the Institute for Fiscal Studies; international comparisons via the Finnish Centre for Pensions.

Five age milestones do most of the work in the United States. Hitting each one unlocks a different category of savings or coverage, so it helps to know them in order rather than waiting until a birthday passes and missing the window.

If you are an adult child tracking these dates for a parent, the practical move is to flag age 64 and three months on the calendar, because the Medicare initial enrollment window opens three months before the 65th birthday.

Before you compare ages, it helps to know the four lenses experts use. Each one answers a different question, and most disagreements about “when someone is old” come from people using different lenses without realizing it.

Because a 65-year-old and a 90-year-old have little in common medically, gerontologists split the senior population into three sub-groups. The young-old (roughly 60 to 74) are typically active and independent. The middle-old (roughly 75 to 84) often begin managing mild chronic conditions and sensory changes. The oldest-old (85 and up) are more frequently associated with frailty and a higher reliance on long-term careA range of services and supports to meet health or personal care needs over an extended period of ti....

Crossing 65 sharply raises the statistical odds of managing a chronic condition. Authoritative data published in 2025 shows that 93% of adults aged 65 and older live with at least one chronic condition, and 79% manage two or more, according to the National Council on Aging. That reality is a major reason Medicare eligibility is tied to this age.

The most common conditions among adults 65 and older are high blood pressure (61%), high cholesterol (55%), and arthritisAn inflammation of the joints that causes pain and stiffness and is more common in older adults. (51%), followed by obesityExcessive body fat accumulation that presents a high risk for various diseases, such as diabetes and..., diabetesA chronic condition that affects the way the body processes blood sugar (glucose), requiring ongoing..., and cancerA disease in which some of the body's cells grow uncontrollably and spread to other parts of the bod.... These are the conditions that drive most senior healthcare spending and shape which Medicare plan structure makes sense for a given person.

Health risk is not only physical. A national poll found that about 37% of older adults aged 50 to 80 experience loneliness and 34% report feeling socially isolated. The National Institute on Aging links prolonged loneliness to higher rates of heart diseaseA broad term for a range of diseases affecting the heart and blood vessels, often related to atheros..., accelerated cognitive declineThe gradual loss of cognitive function, which can include memory impairment, difficulty with decisio..., and increased risk of dementiaA chronic disorder characterized by a decline in cognitive function beyond what might be expected fr.... Staying socially connected is not a soft recommendation. It is a measurable health intervention.

The same age chart serves two readers differently. If you are approaching these ages yourself, the milestones are a savings calendar. If you are an adult child planning for a parent, they are a coordination tool. Both readers benefit from treating the ages as triggers for specific actions rather than abstract labels.

In our experience helping families, the costliest mistakes happen at age 65. People assume Medicare enrollment is automatic for everyone, but unless you are already drawing Social Security, you usually have to sign up yourself during a seven-month window around your 65th birthday. Miss it, and Part B premiums can carry a permanent late penalty. The second most common mistake is leaving money on the table between 50 and 64, when discounts exist but go unclaimed because people do not feel “old enough” to ask.

For families, the most useful framing is to separate the conversation about benefits from the conversation about aging. A parent may resist being called a senior while happily accepting a program that lowers their Medicare premiums. Lead with the concrete benefit, not the label. If income is tight, many seniors qualify for programs that reduce healthcare and living costs without realizing it.

There is no single birthday that turns you into a senior citizen. Seniorhood is a series of doors that open at different ages: discounts around 50 to 55, global recognition and travel perks at 60, early Social Security at 62, Medicare at 65, and full retirement benefits at 67. The smart approach is to treat each age as a checklist item, not an identity.

As of 2026, the most important shift is that full retirement age has reached 67 for everyone born in 1960 or later, even as Medicare stays at 65. Knowing that two-year gap, and planning around it, is one of the highest-value financial moves available to anyone in their early sixties.

When you are ready to turn these ages into actual savings, start with our complete guide to government benefits for seniors, which takes you from eligibility all the way through a submitted application.

Sometimes, yes. Age 55 is a common commercial and housing threshold rather than a government one. Many restaurants and retailers offer senior discounts at 55, and U.S. law allows “55 and older” age-restricted communities. But you will not qualify for Medicare or full Social Security at 55.

Age 65 unlocks the most valuable single benefit, federal Medicare health insurance. However, the broadest set of benefits accumulates across several ages: discounts at 50 to 55, transit and travel perks at 60, early Social Security at 62, and Medicare at 65.

Age 65 is when Medicare health coverage begins. Age 67 is the full Social Security retirement age for anyone born in 1960 or later. You can start Social Security as early as 62, but claiming before 67 permanently reduces your monthly benefit by up to about 30%.

In the United States, no. Social Security and Medicare ages are identical regardless of sex. Some countries historically used different pension ages by sex, but most, including the United Kingdom, have moved to a single gender-neutral age.

Both the U.S. and the U.K. are completing scheduled increases in their full retirement and state pension ages because people are living longer and governments are managing program costs. The U.S. full retirement age reaches 67 in 2026, and the U.K. is phasing its state pension age up to 67 by 2028.

Yes, and most people start well before 65. AARP is focused on adults 50+, but membership is open to anyone 18 or older. Some AARP benefits, especially insurance-related products, may still be age-restricted.